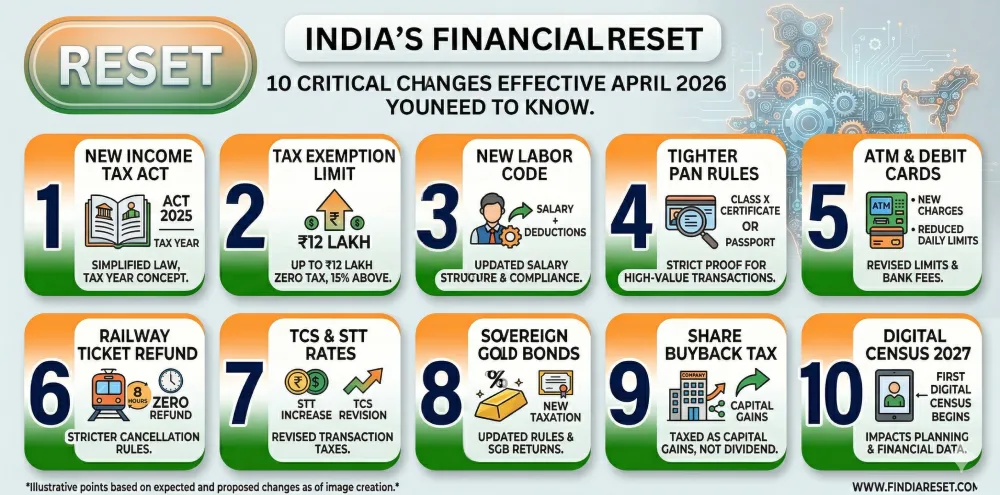

India’s Financial Reset: As of April 1, 2026, India has embraced substantial legislative updates aimed at enhancing its financial framework. At the forefront of these changes is the introduction of the Income Tax Act of 2025, which replaces the decades-old Income Tax Act of 1961. This overhaul is not merely a change of text; it marks a significant shift in how income tax is perceived, administered, and applied across the nation.

The new Act reflects a commitment to modernizing the tax system, streamlining processes and reducing the compliance burden on taxpayers. The previously complex terms such as ‘assessment year’ and ‘previous year’ have been replaced with a more user-friendly ‘tax year’ terminology. This is intended to simplify tax administration for citizens and provides a clearer understanding of financial obligations during the specified periods.

Moreover, the reforms emphasize the importance of enhancing savings opportunities for individuals and businesses alike. By simplifying tax compliance, the government aims to encourage more individuals to engage with the formal economy, thereby potentially increasing tax revenue and promoting fairer tax distribution. This effort not only seeks to boost national revenue but also aspires to foster a more inclusive financial system that benefits a wider section of society.

In this new era of governance, the focus is clearly on making taxation more approachable. By replacing outdated terminologies with clearer concepts, the government is also signaling its responsiveness to the evolving economic landscape. The reforms are expected to set the stage for a more transparent and efficient tax regime, aiming to facilitate growth, enhance governance, and ultimately support the broader economic ambitions of the country.

Major Tax Reforms

The new Income Tax Act of 2025 introduces significant changes aimed at modernizing India’s tax structure, promoting compliance, and alleviating the tax burden on individuals and businesses. One of the most noteworthy alterations is the revised tax rates, which are designed to streamline the previous tax brackets and provide a more equitable system. The government has reduced the number of tax brackets, simplifying the filing process for taxpayers. This reform aims to ensure that taxpayers can easily determine their tax obligations while fostering a sense of fairness in the taxation system.

In addition to the revised tax rates, crucial modifications have been made regarding exemptions and deductions. The government has increased the limits for certain exemptions, particularly for middle-income earners. This adjustment is intended to enhance disposable income for individuals, ultimately spurring consumer spending and stimulating economic growth. Furthermore, specific deductions have been restructured to better align with contemporary financial practices, making it easier for taxpayers to claim benefits without extensive documentation.

Another significant aspect of the reformed tax framework is the introduction of simplified compliance mechanisms for businesses. The Act emphasizes the digitalization of tax processes, promoting a more efficient and transparent system that minimizes administrative burdens on businesses, especially small and medium enterprises (SMEs). By leveraging technology, the government aims to enhance compliance rates, thereby increasing overall tax revenue while reducing the efforts required from taxpayers.

Overall, these major tax reforms signify the government’s commitment to establishing a more efficient and fair tax culture in India. The changes empower both individuals and businesses while fostering an environment conducive to economic growth. As taxpayers adapt to these new regulations, it is essential for them to stay informed and consider their financial strategies in light of the evolving tax landscape.

Introduction of the Tax Year Concept

Beginning in April 2026, India will implement a significant modification to its fiscal landscape by introducing the concept of the ‘tax year’. This change marks a shift from the existing financial year system to a tax year structure, which will have substantial implications for both individual and corporate taxpayers. The adoption of the tax year concept aligns India’s tax system more closely with international practices, thereby aiming to enhance compliance and administrative efficiency.

In practical terms, the transition to a tax year means that the annual period for calculating income tax liability will now run from April 1st to March 31st of the following year. This shift necessitates a careful reevaluation of tax filing timelines and payment deadlines for all taxpayers. For individuals and businesses, the prior financial year will no longer serve as the basis for tax reporting; instead, adherence to the new tax year will be essential to avoid penalties and ensure accurate compliance.

Taxpayers will need to adjust their financial planning strategies to accommodate this change. For instance, businesses will have to align their accounting practices, reconciliation processes, and reporting schedules with the new timeline. Individuals, too, would be wise to revisit their tax saving investments and deductions, ensuring that they are adequately prepared for the altered filing periods. This comprehensive understanding of the tax year concept will be vital in facilitating a smoother transition and in optimizing tax liabilities effectively.

As Indian taxpayers prepare for this new paradigm, it is crucial that they stay informed about how the tax year affects their obligations, especially concerning deadlines for filing returns and making tax payments. By doing so, both individuals and corporations can ensure compliance and minimize any disruptions in their tax planning efforts.

Revising Income Tax Slabs

The Income Tax Act of 2025 has introduced significant changes to income tax slabs, providing a refreshed structure that aims to enhance taxpayer benefits and adjust to the evolving economic landscape. These revisions are designed to simplify tax compliance and ensure a fairer distribution of the tax burden. The new income tax slabs will take effect in April 2026, allowing taxpayers ample time to understand and adapt to the changes.

Under the revised income tax slabs, India will see a more progressive tax structure that aims to provide relief to the middle-income earners while ensuring higher contributions from wealthier individuals. For example, the new tax brackets might lower the tax rate for individuals earning between INR 5,00,000 to INR 10,00,000, while slightly increasing the rates for those earning above INR 10,00,000. This change is expected to promote disposable income and encourage spending among the lower and middle-income groups.

One of the main rationales for these changes is to increase compliance and transparency within the tax system. The previous tax slabs often created confusion, with multiple deductions and exemptions that complicated tax calculations. The streamlined approach of the new income tax slabs reduces the complexity and aims to encourage more citizens to participate in formal financial systems. Furthermore, it is anticipated that these revisions will help reduce tax evasion, leading to an increase in government revenue.

Comparatively, previous tax slabs had several key points of contention, particularly concerning the burden on the middle class. The revised slabs are expected to address these grievances, allowing for a more balanced approach to taxation. Taxpayers should take note of these changes, as they can significantly influence individual tax liabilities. With a clearer structure, individuals can better plan their finances, investments, and future expenses accordingly.

Enhanced Deductions for Individuals and Corporates

With the impending financial reset in April 2026, several enhanced deductions are set to take center stage for both individuals and corporations. These changes aim to alleviate tax burdens and encourage investment in various sectors. For individuals, deductions on specific investments have been increased significantly. Individuals can now benefit from higher deductions on premiums for health insurance policies, contributing to their overall tax savings. The eligibility for these enhanced deductions varies, often depending on the taxpayer’s income level and the nature of the expenses incurred.

For corporates, the landscape will undergo substantial modifications, particularly with respect to deductions associated with research and development (R&D). Companies investing in innovation and technological advancement can expect greater tax incentives. This shift not only fosters a culture of innovation but also aligns with the government’s objective to enhance India’s competitive edge in the global market.

In addition, corporations focusing on sustainable practices will find new avenues for increased deductions. Expenses related to green initiatives, such as renewable energy installations or environmentally friendly business practices, may now qualify for substantial tax relief. These measures aim to promote corporate responsibility towards the environment, which is becoming increasingly important in today’s economic climate.

To maximize tax savings through these enhanced deductions, individuals and corporates must maintain diligent records of their expenses and ensure compliance with the updated tax regulations. Consulting with tax professionals can provide personalized insights and strategies, ultimately minimizing overall tax liabilities while harnessing the full benefits of the new regulations.

Changes in Corporate Tax Policy

The new Income Tax Act introduces significant modifications to the corporate tax landscape in India, which take effect in April 2026. Aimed primarily at enhancing the attractiveness of the investment environment, these reforms are designed to foster growth among businesses while ensuring compliance with the evolving tax framework.

One of the key changes includes a reduction in the corporate tax rate for new manufacturing companies. This adjustment aims to incentivize domestic and foreign investments in manufacturing by decreasing the overall tax burden. As companies will now be taxed at a lower rate, the expectation is that this will drive economic expansion, job creation, and technological advancement.

Additionally, the revised tax policy introduces incentives for research and development (R&D) expenditures. Corporations that invest in R&D will now enjoy more favorable tax treatment, facilitating innovation and encouraging investment in high-tech projects. This move is anticipated to position India as a hub for advanced manufacturing and services, elevating its global competitiveness.

Furthermore, to simplify compliance, the government is implementing a new digital tax administration system. This initiative is intended to streamline processes such as filing returns, payment of taxes, and maintaining records. Corporations need to familiarize themselves with these technological tools to ensure efficient and accurate compliance with tax regulations.

Enterprises must also be aware of the updates concerning transfer pricing regulations. Stricter norms governing transactions between related entities are designed to curb tax avoidance and ensure fair taxation among multinational corporations. It is essential for companies to assess their transfer pricing strategies and align them with the new guidelines to avoid potential penalties.

In conclusion, the changes in corporate tax policy represent a pivotal shift towards creating a more conducive environment for business growth. Corporations need to stay informed and adapt to these alterations to effectively navigate the complexities of the new tax landscape while maximizing potential benefits.

Impact on GST and Indirect Taxes

The financial reforms effective April 2026 bring about significant changes to the Goods and Services Tax (GST) and other indirect taxes in India. These reforms are designed to enhance the efficiency of the indirect tax system while simplifying compliance for businesses and individuals. One of the primary objectives is to create a more streamlined and transparent taxation framework that aligns with the newly established income tax structure.

With the introduction of new guidelines, businesses will experience modifications in their compliance obligations. These updates are expected to make the filing of GST returns more straightforward and less time-consuming. The aim is to reduce the regulatory burden on small and medium-sized enterprises, which often struggle with the complexity of the current system. The reform intends to ease the reporting process and promote timely submissions, thereby minimizing the chances of penalties resulting from non-compliance.

Moreover, the interconnectedness of GST with the revised income tax framework is noteworthy. The new reforms are expected to facilitate a holistic approach to tax collection, encouraging tax compliance and governance. By integrating GST with enhanced income tax measures, the government aims to capture a broader spectrum of economic activity and ensure that a higher proportion of tax revenues is collected more effectively. This synergy is anticipated to not only bolster government revenues but also contribute to a more equitable taxation model.

Additionally, adjustments to the GST rate structure may occur in line with broader economic goals. Such changes are likely to be aimed at stabilizing market prices, ensuring that consumers are not disproportionately affected by the tax regime. Overall, the reformulation of GST and indirect taxes signifies a pivotal step towards a more organized financial landscape in India, setting the stage for long-term economic growth.

Fostering Digital Payments and E-Filing

The Indian government is making significant strides towards promoting digital payments and facilitating e-filing of returns as part of its broader financial reforms implemented in April 2026. These initiatives aim to modernize the taxation regime and enhance compliance while streamlining the financial processes for taxpayers. Notably, the adoption of digital payment systems provides a multitude of benefits such as increased efficiency, transparency, and security.

By encouraging the use of digital payment methods, the government is not only simplifying transactions for taxpayers but also reducing the reliance on cash, which is often associated with a higher risk of tax evasion. Digital payments enable faster processing of transactions and decrease the administrative burden on tax authorities. Moreover, they foster a transparent financial environment that helps in tracking income and ensuring appropriate tax collection.

E-filing further complements this shift towards digitization. By allowing taxpayers to file their returns online, the process becomes more convenient and accessible. Taxpayers can complete their submissions from the comfort of their homes, thus eliminating the need for physical trips to tax offices. The integration of e-filing with digital payment systems creates a seamless experience whereby due taxes can be paid electronically during or after the filing process.

Additionally, embracing these technologies not only benefits taxpayers but also empowers the government to harness data analytics effectively. This fosters better decision-making, enhances compliance monitoring, and minimizes the possibilities of fraud. As a result, a robust digital infrastructure for payments and e-filing lays the groundwork for increased public trust in the tax system and promotes voluntary compliance among taxpayers.

In conclusion, the emphasis on digital payments and e-filing marks a crucial step in India’s financial reset, signifying a forward-thinking approach to enhance the overall tax experience for individuals and businesses alike.

Conclusion

As we approach April 2026, the critical changes introduced in India’s financial landscape promise to reshape the way individuals and businesses engage with their financial strategies. From modifications to tax structures to the amendments in the regulatory frameworks, these reforms aim to enhance transparency and efficiency within the financial system. Each of the changes outlined in this blog post marks a significant step towards modernizing India’s financial practices, fostering greater compliance and a more robust economic environment.

Staying informed about these developments is essential for both personal and business finance management. As regulations evolve, individuals must adapt their financial plans and strategies accordingly to ensure compliance and optimization of their resources. Understanding the implications of each change, whether it relates to taxation, investment guidelines, or compliance requirements, will empower stakeholders to make informed decisions and maximize their financial outcomes.

In this rapidly changing financial scenario, leveraging tools and resources to remain updated is crucial. Engaging with financial advisors, participating in seminars, and utilizing credible information platforms can provide deeper insights into navigating the complexities introduced by these reforms. Being proactive in seeking knowledge and adapting to the new environment will be essential for success.

In conclusion, embracing the upcoming changes and developments within India’s financial framework is not just a necessity but a strategic advantage. By understanding and anticipating the impact of these reforms on financial behaviors, individuals and businesses can better position themselves for the future. Staying informed and adaptable will ultimately enhance one’s ability to thrive in an evolving financial ecosystem.